Finance Principles of Accounting

Basis of Accounting

Cash Basis of accounting, recognizing transactions and events when related cash amounts are received and dispersed. The cash basis of accounting is a basis that differs from U.S. Generally Accepted Accounting Principles. The cash basis of accounting does not give effect to accounts receivable, accounts payable, and accrued items.

Current financial resources measurement focus is where the aim of a set of financial statements is to report the near term (current) inflows, outflows, and balances of expendable financial resources.

Government-wide Financial Statement

One of the most important questions asked about the City’s finances is, “Is the City as a whole better off or worse off as a result of the year’s activities?” The Cash Basis Statement of Activities and Net Position reports information, which helps answer this question. The government-wide financial statements are designed to provide readers with a broad overview of the City’s finances, in a manner similar to private-sector business.

The Cash Basis Statement of Activities and Net Position is divided into two kinds of activities:

- Governmental Activities include public safety, public works, health and social services, culture and recreation, community and economic development, general government, debt service and capital projects. Property tax and grants both State and Federal finance most of these activities.

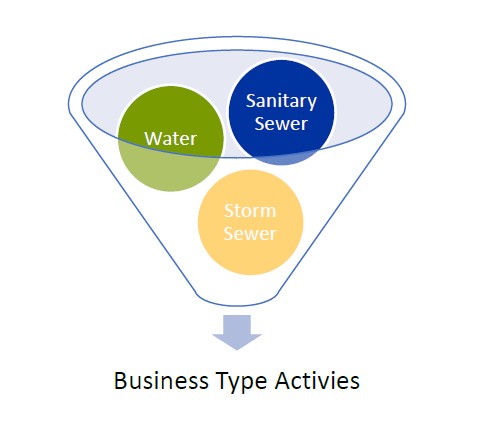

- Business Type Activities include the waterworks, the sanitary sewer system, and the storm water system. These activities are financed primarily by user charges.

Fund Financial Statements

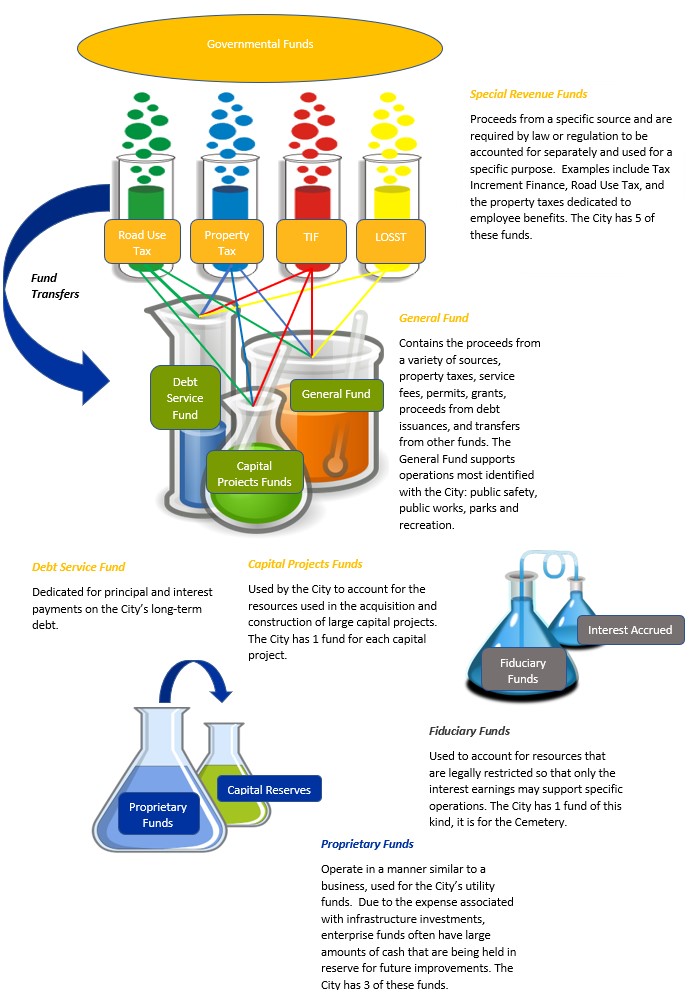

A fund is defined as a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City of Bondurant, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the City’s funds can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds, which are described in further detail below.

Click image to enlarge.